In the pre-investment due diligence phase, management fees represent the largest estimable cost.[1] Therefore, they are an excellent candidate for negotiation. In this analysis, inside-investment-period management fee rates are examined by comparing the base rates found in Limited Partnership Agreements (LPAs) with other contractual obligations. The latter include discounts for size, loyalty, and early close, or could be the result of other negotiation, often articulated in side letters.[2] In the proceeding paragraphs, recent sample data are analyzed to yield insight on discount amounts, discount types, and characteristics of funds that offer discounts.

How large are discounts?

For vintages 2020 through 2023, the median investment-period management fee rate was 1.75%, compared with a median negotiated rate of 1.50%.[3] While 25 basis points (bps) may sound negligible, over the course of the investment period, the absolute value can be significant. For a $100mn commitment over a five-year investment period, 25bps would amount to $1.25mn.

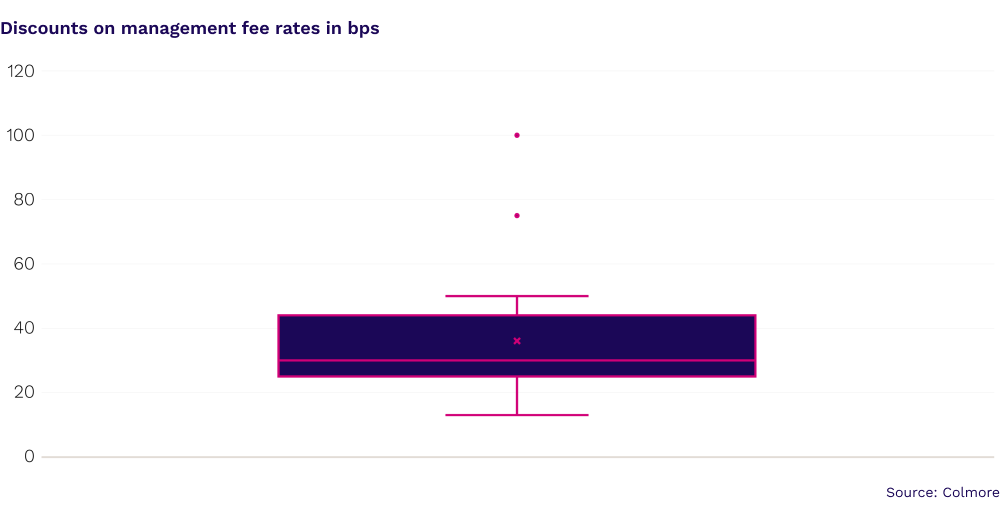

Recent-vintage discounts range in size from 13 to 100bps, with a mean of 36bps and median of 30bps, as shown in Figure 1. About 28% of commitments are granted discounts, which can vary within a fund, based on discount criteria. For example, in a hypothetical growth equity fund, an investor with a £100mn commitment might receive a discount, while an investor with a £25mn commitment may not be eligible for one.

Fig. 1

What kinds of discounts are available?

While GPs may offer discounts for any reason, the three most common are outlined here: size, timing, and loyalty.

Size

The most common discounts relate to commitment size. In the sample data, commitments were divided into four size categories: <$100mn, $100-199mn, $200-299mn, and $300mn+. As observed in Figure 2, the largest commitments, of $300mn+, received the lion’s share of discounts, at over 52%. As commitments decreased in size, so did the incidence of discounts. In fact, while the <$100mn category included the most commitments, it had the lowest incidence of discounts. This correlation between commitment size and incidence of discount likely reflects the relative back office and fundraising burdens on GPs.

Fig. 2

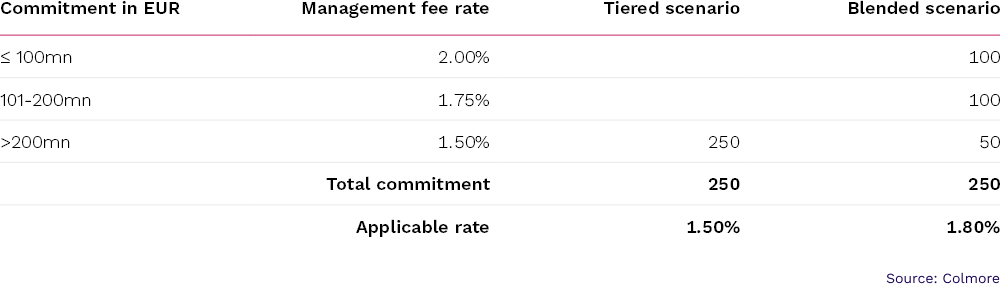

Size discounts frequently take one of two forms: tiered or blended.

- Tiered rates

Here, one rate is ascribed to any commitment within a given range. For example, 2% could apply to investors with a commitment of up to EUR 100mn, 1.75% to those with a commitment of between EUR 100mn and EUR 200mn, and 1.5% to those with a commitment of over EUR 200mn. - Blended rates

For blended rates similar ranges can apply, but an LP pays the rate that applies to each tranche of its commitment. For example, as seen in Table 1, for an investor with a EUR 250mn commitment and the same ranges as above, the rate would be weighted at 40% to the lower two rates and 20% to the top tier, for an effective rate of 1.8%. Under the tiered rate above, the same investor would have paid 1.5%. Thus, the blended form results in a higher rate than the tiered form, which is less favorable to an LP.

Table 1: Comparison of tiered and blended management fee rates for a EUR 250 commitment

The size of a commitment can be such an important consideration that GPs will assess fees for smaller commitments. Typically, this applies to commitments below $10mn and takes the form of additional basis points tacked onto the base management fee rate. Where applicable, the resulting small commitment fee runs around 25bps.

Timing

Another common discount relates to timing. Early closing discounts are extended to investors who commit to a fund before a specified date, often at an early or initial fund close. In this case, GPs incentivize LPs to commit early, injecting more certainty into fundraising and earlier in the cycle. Alternatively, an investor might be offered a period with no fee, or a fee holiday. While this does not lower the fee rate, it effectively lowers the total management fee paid by reducing the length of the management fee period.

Loyalty

Loyalty discounts can be extended to investors that have previously invested with a given fund manager. In some cases, the discount increases based on the number of previous funds in which an LP has invested. Such discounts incentivize a continued relationship between an LP and GP and are more common among smaller, newer fund managers.

What kind of funds give discounts?

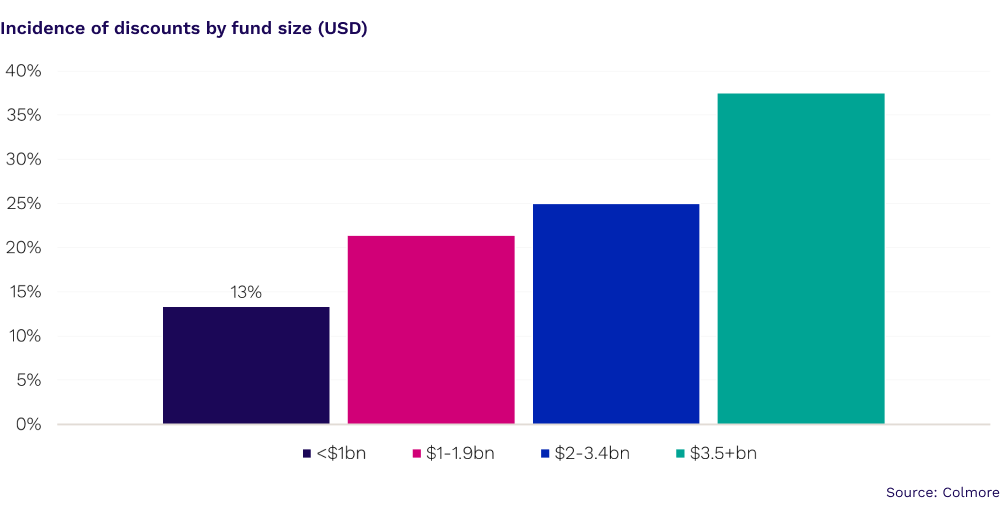

Discounts occur unevenly across fund size and strategy. In the recent-vintage sample, the larger the fund size, the more frequently a discounted management fee rate is applied. Of the four categories of fund size, the largest, or $3.5bn+ category, shows the highest incidence of discounts. As shown in Figure 3, 38% of the commitments to the largest funds were granted discounts. This is nearly three times those granted to commitments to the smallest funds — only 13% of commitments to funds of less than $1bn were given management fee discounts. The direct relationship between fund size and management fee rate discount is likely to reflect a larger GP’s flexibility to offer discounts because its base of commitments is broader.

Fig. 3

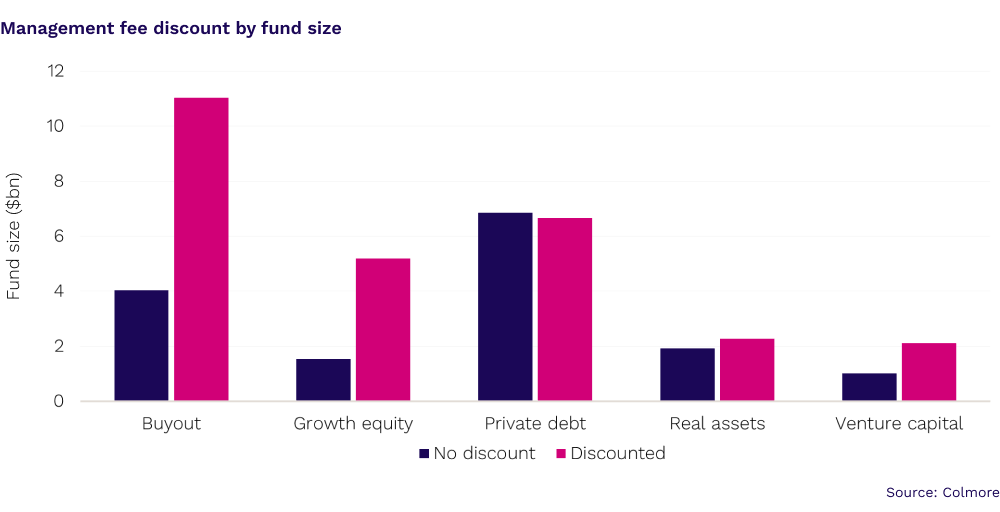

Across fund type, the size of a fund is associated with whether management fees are discounted or not. In Figure 4, the median fund size for each grouping is shown in two categories:

- No discount

- Discounted

In four of the five groupings, the funds that offer management fee discounts are larger than those that do not. The most notable examples of this were in buyout and growth equity funds, in which the discounting funds were 3 time the size of the non-discounting funds.

Fig. 4

What kind of funds don’t give discounts?

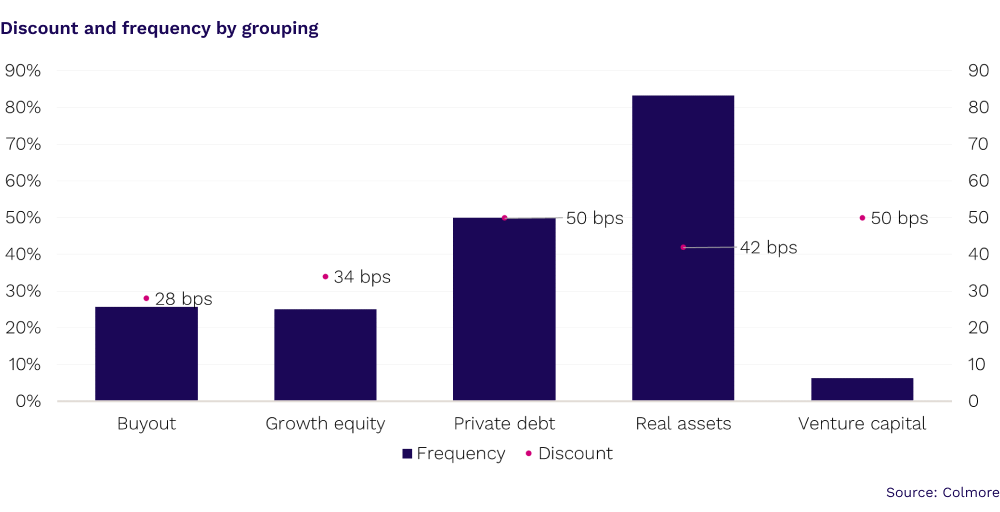

Not all funds offer management fee discounts. As seen in Figure 5, venture capital (VC) funds do not typically extend discounts, with only about 6% of VC commitments enjoying them. The data also show that growth equity and buyout were unlikely to offer discounted management fee rates, about 25% and 26%, respectively. And when growth equity and buyout funds offer discounts, they were the lowest, 28 and 34bps, respectively.

Fig. 5

Conclusion

In conclusion, roughly 72% of commitments to recent-vintage funds do not receive discounts to investment-period management fee rates. When commitments receive discounts, they are often associated with larger funds and larger commitments, with some variability across groupings. As the fundraising climate evolves, management fees could be a negotiating point from a variety of angles.

[1] Investment-period gross management fees can be estimated based on legal documents and historical data. Due to variables such as investment period length, which in many cases, depend on external factors, such fees can be estimated within a range at a reasonable level of certainty.

[2] All data herein are taken from the Colmore universe, an anonymized database. The funds examined in this analysis are from vintages 2020-2023 and they comprise the groupings of buyout (BO), growth equity (GE), venture capital (VC), real assets (RA), and private debt (PD). They exclude real estate, co-investments, secondaries, SMAs, fund-of-funds, and funds with bifurcated management fee structures. The median commitment is $125mn. Typical LPs include sovereign wealth funds, pension funds, and family offices.

[3] Ibid.